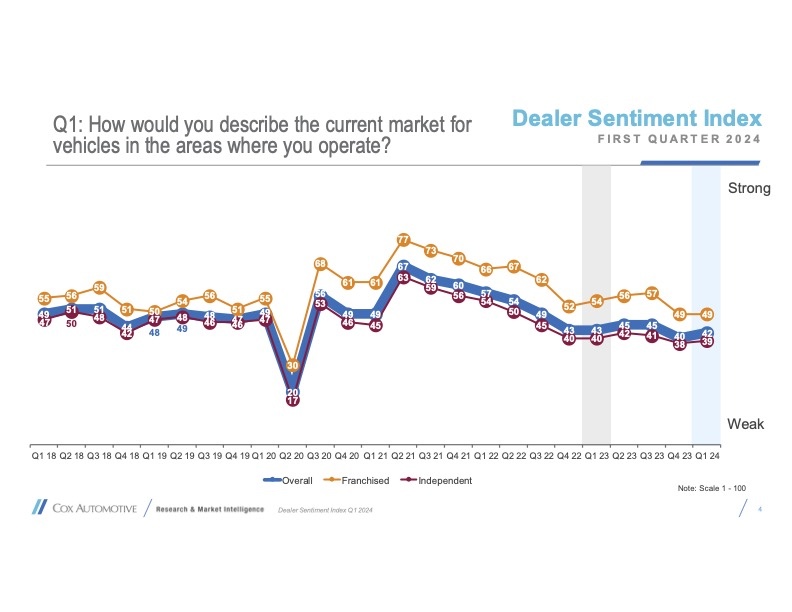

A recent survey found dealers more optimistic than they were at the end of last year—but are still worried about major economic headwinds consumers are facing.

The recently released Cox Automotive Dealer Sentiment Index (CADSI) resulted in a score of 42 out of 100 when it came to dealers view of the U.S. economy, up three percentage points from 2023 Q4.

The franchised dealers’ score of 46 held steady quarter over quarter, whereas independent dealers saw an improvement, moving up from 36 to 40.

Interest Rates

The key factors cited as concerning to dealers are interest rates, the economy, and market conditions. But all three factors decreased compared to Q4 2023.

Interest rates are the biggest factor cited by franchised and independent dealers, with 62 percent of dealers citing interest rates as the top factor in the first three months of 2024. That is down from three percentage points from the last quarter.

But to show the impact it has had on the industry, Cox noted only five percent of dealers cited interested rates as holding back business two years earlier.

Improving Economy

The overall economy was next on the list at 55%, down from the dealers citing it 61 percent last quarter. Market conditions fell eight percentage points to 40 percent in Q1 from 2023 Q4.

Here is a list of the top 10 factors dealers said held back business in Q1 2024:

- Interest Rates 55%

- Economy 54%

- Market Conditions 42%

- Political Climate 25%

- Expenses 29%

- Credit Availability for Consumers 326%

- Limited Inventory 43%

- Consumer Confidence 28%

- Weather 13%

- Competition 12%

Spring Bounce

Despite many of the factors driving the current market index remaining subpar, the market outlook index improved significantly to 51 in Q1 from 41 last quarter. The market outlook index, which queries dealers about expectations for the vehicle market three months from now, historically enjoys a ‘spring bounce’ as automobile dealers look to the spring selling season.

The new-vehicles sales index improved a percentage point to 52, but down from 57 one year ago. Likewise, the used-vehicle sales index increased the same one percent to 40, but declining from 44 a year ago and well below the long-term index average of 50.

For franchised dealers, the used-vehicle sales index held steady near a record low of 51 in Q1. For independent dealers, the used-vehicle sales index increased by one point but remains well below longer-term averages.