Organizations frequently embark on various cost reduction initiatives across their enterprises. Some organizations have purchasing departments and their role is typically to get the right product or service, to the right location, at the right time at the best cost. In either case, whether your organization is centralized with a purchasing department or decentralized with various departments working on cost savings initiatives, one common frustration will normally occur. Where are the cost savings? How come we can’t see them? Are they really there? Frustration can occur unless some visibility is shed on the challenges inherent in this process.

Profit and Loss Statement Challenge

Most of us would assume that cost savings generated would be easily identified on the profit and loss or P&L statement generated each month. Any reduction in price and spend should be easy to identify on the P&L right? Wrong!

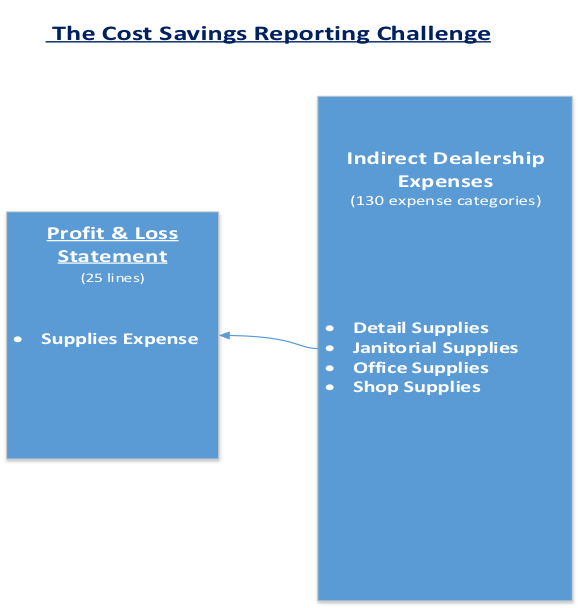

The typical P&L statement is a summary document. While all P&Ls are summary documents, they typically contain about 25 lines of expense to review. The reality however is that most companies spend dollars in between 60 to 130 expense categories depending upon the industry. So, how are those expense categories represented on the typical P&L? They are typically summarized into the most appropriate line on the P&L.

Remember, supplies and services might number as many as 130 expense categories in your organization, so the spend and savings you have obtained are going to be aggregated with many other categories represented in the summary P&L document which is represented by about 25 lines on the document.

Example: Why Don’t I See the Office Supply Savings?

Your organization reduced your office supply pricing by 25% and expect to see average savings of $24,000 per year on office supplies. You have verified that all employees are using the designated supplier, at the new prices, and the suppliers are selling the product at the agreed pricing. So, the office supply spend is now blended into a category on your P&L listed as “Supplies.” The spend for “Supplies” this month did not decrease, but actually increased…how can that be? There are a number of possible explanations including the following:

Blending Problem: Shop supply spend or some other spend under this Supplies category on the P&L may have increased this month, hiding the effect and benefits of the new office supply savings.

Consumption Problem: While the pricing of office supplies has improved by 25%, it may be that your consumption of those supplies increased…using more product than you did before

Supplier and Mix Problem: While the negotiated pricing is in place for designated items, your employees might be purchasing the “wrong” items…they might be ordering the brass stapler at $25.00 versus the steel stapler at $5.00. They might also be using the wrong supplier. Or, said a different way, you have an internal compliance issue.

If any of these scenarios occur, the cost savings you achieved are legitimate, but the issue is either a reporting problem (P&L) or a management issue (usage or compliance).

Audits: The Best Way to Validate Cost Savings

So far, we have reviewed the spend management elements that will yield long term, sustainable cost savings. We understand that negotiated cost savings can and will be masked by the construction of the P&L statement given the summary nature of the document. We have also discovered that many elements of a cost savings initiative need to be controlled to ensure that the savings actually materialize. So, what then is the best way to validate cost savings for supplies and services across an organization?

Category Audits Will Validate Cost Savings

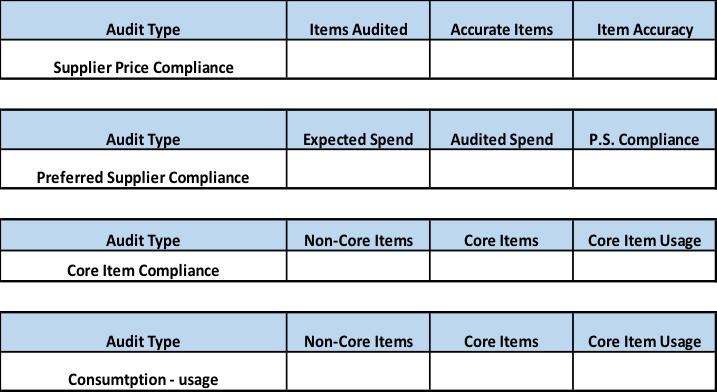

A category audit can be used to validate cost savings in any expense. There are four components of a category audit, all of which are critical to the integrity of the audit. Cost savings will be achieved if four things occur: the pricing is right, the right supplier is used, consumption levels are correctly realized and finally, if the right items are being purchased. If those things happen, then the savings will occur regardless of whether it can be seen on the P&L or not. Those audit elements are as follows:

Supplier Compliance: Reports on supplier price and business-term compliance against expectations or the original contract.

Client Compliance: This part of the audit reports on whether the organization is using the right supplier, the designated or preferred supplier. This audit will also validate whether the expected spend is observed. This is the money question. Is our overall spend lower and meeting our original projections or not? If not, the organization could be using suppliers other than those designated and that needs to be determined and corrected.

Item Compliance: This part of the audit verifies whether the right items are being consumed… the high usage items that were negotiated and recommended. These “core” items or selected services should be consumed versus the higher cost alternatives that might be available.

Consumption: If the organization consumes more of a service or a supply, the costs will increase and cost savings will be hard to find. Obviously, if business levels increase, greater consumption is justified and welcomed. If however, business is flat or declining, consumption should follow the same trajectory.

If your category audit consists of these four components… rest assured, your cost savings are there. The savings are real and measurable and you just proved it with this simple audit. Even though the savings are hidden or buried in various financials… you can’t dispute that prices are lower, terms are better, the spend in that category is lower, and the limited spend dollars are being used with the most cost effective items.

Summary

This article began with a question, “Where are the cost savings?” This is a question that many executives ask of their teams and some ask of their own purchasing departments from time to time.

Traditional financial documents such as the P&L can rarely be used to identify or validate cost savings because of the summary nature of the document itself. With over 130 expense categories jammed into 25 or so lines on a typical P&L, the challenge of validating savings might appear daunting. This problem can be overcome with a series of post implementation audits. If those audits focus on price accuracy, use of the proper supplier, checking in on forecasted spend and consumption and if the correct items are used…well then you have validated your cost savings and done a good job for your organization. When management asks “Where are the cost savings?” you can point to your audit results as proof positive that not only are pricing and terms better, but employee behavior and decisions have improved as well, leading to sustainable cost savings today and into the future.